Vision Coverage

Overview

The State of Rhode Island offers eligible active employees two options for vision coverage—Anchor Vision and Anchor Vision Plus. Both plans are administered by the Vision Service Plan (VSP).

Coverage Details

Key Plan Features

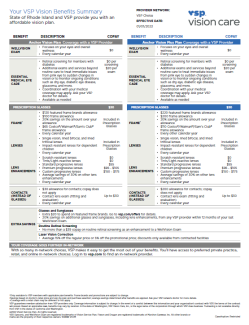

Anchor Vision and Anchor Vision Plus both offer preventive care coverage and an allowance for frames and contacts. Anchor Vision is a base plan, but Anchor Vision Plus is a "buy-up" option that offer bigger allowances.

Under both Anchor vision plans:

- Dependents up to age 26 are eligible to enroll.

- Both plan options offer benefits in- and out-of-network. However, the State encourages you to visit a VSP participating provider to receive the greatest coverage. To find a provider near you, visit www.vsp.com.

- VSP does not issue ID cards, but you may print one out after registering/logging into your account on www.vsp.com. Your ID number is your Social Security Number. At your appointment, tell your doctor that you are a member of VSP in order for him/her to verify your VSP eligibility.

Eyeconic®

VSP offers an online, in-network eyewear store called “Eyeconic,” exclusively for VSP members. Eyeconic has a huge selection of contact lenses and designer frames at low prices. In fact, if you find a lower price, they will refund you the difference. There’s a virtual tryon feature, and shipping and returns are free. Eyeconic is also the ONLY website considered in-network for online contact lens purchases. Visit www.eyeconic.com to start shopping.

How Does the "Buy-Up" Option Work?

You can elect to pay a higher premium (co-share) to receive more vision coverage (higher allowances) under the "buy-up" option, Anchor Vision Plus. Keep in mind, however, that the State’s contribution towards the cost of your coverage is the same regardless of whether you elect the base or the buy-up option.

Plan Comparison

Click on the chart below to see how Anchor Vision and Anchor Vision Plus compare across specific coverages.

Plan Documents

Need Help Choosing Your Plan?

Visit the virtual benefits fair and the Decision Support page for tools such as ALEX® and benefits videos & presentations that can help you better understand your plan options and make the best choice for you and your family.

Any State employee that satisfies all of the following criteria is eligible to enroll:

- Holds a non-seasonal position

- Scheduled to work at least 20 hours per week

- Not on leave without pay (LWOP)

The following dependents are also eligible for enrollment:

- Spouse

- Common Law Spouse

- Married federal income tax filing status – The IRS allows common law spouses to file their taxes married-joint if they live in a state like Rhode Island that recognizes common law marriage. Because common law spouses receive the same favorable pre-tax benefits treatment as spouses that can provide a marriage certificate, employees wishing to cover a dependent as a common law spouse must provide a copy of their most recent federal income tax filing showing married-joint or married-separate tax filing status. In the absence of such a tax filing status, the dependent may still be eligible for coverage as a domestic partner.

- Domestic partner

- Imputed Income – Pursuant to federal guidance, under the State employee health plan the fair market value of any health coverage extended to a domestic partner will be imputed to you as income on your paycheck. This imputed income would be added to the your federal taxable gross wages, State taxable gross wages and social security taxable wages. Additionally, any coverage provided to a domestic partner is paid for on an after-tax basis. You will have additional tax withholdings based on the imputed income and the increased taxable wages due to the reduction in pre-tax contribution. The amount of imputed income is generally around $200 per pay period for medical/prescription, dental and vision coverage, and the amount of the reduction in pre-tax contribution is generally around $100 for the same coverage. This means that you will have additional tax withholdings based on approximately $300 per pay period. Generally, the additional tax withholdings will be in the same proportion as your normal tax withholdings are to your regular pay.

- Marriage – If you and your domestic partner get married, it is YOUR responsibility to inform the Office of Employee Benefits in writing immediately. Your failure to do so will prevent you from obtaining refunds of additional tax withholdings based on imputed income. The Office of Employee Benefits will not coordinate such refunds if it is not notified within 31 days of the date of the marriage.

- Termination of domestic partnership – If your domestic partnership ends, you will not be able to drop your domestic partner from your coverage until open enrollment (for effect January 1 of the following year) unless your domestic partner experiences a qualifying status change.

- Addition of new domestic partner – If you drop your domestic partner, you will not be able to add a new domestic partner for at least 6 months, assuming your new domestic partner meets all eligibility requirements.

- Children* (Up to the end of the month in which they reach age 26. At that time, coverage will be automatically terminated with no action required by the employee, and COBRA continuation coverage will be offered.)

* Children of domestic partners are not eligible unless they are also the natural/adopted child of the employee, or the employee has legal guardianship.

Enrollment Periods

Employees may enroll in vision coverage during one of the following periods:

- Within 31 days of date of hire or a qualifying status change

- Open enrollment

Enrollment Process

Step 1: Do your research!

- Visit the virtual benefits fair to watch recorded BCBSRI and CVS Caremark presentations.

- Review your past medical and prescription expenses and think about the coverage you need in the future, then talk to ALEX.

- Watch the Your Dental & Vision Plan Options whiteboard video posted above

- Review the detailed benefits information on the "Coverage Information" tab of this page

Step 2: Enroll!

Visit the Benefits Enrollment page for all the guidance you’ll need to enroll in benefits or make changes to existing benefits elections.

See below for 2025 premium rates—i.e., your co-shares. Premium co-shares for prior years can also be found below.

A co-share is the amount that is deducted from your pay each pay period for your coverage. It is your “share” of the overall plan cost. Co-shares vary by individual vs. family coverage, as well as by annual salary and full-time/part-time status. Co-shares listed here are for classified and unclassified State employees only. Non-classified union & non-union employees working in higher ed should refer to their college/university website (URI, RIC, CCRI) for their co-shares.

Co-share amounts are determined as a percentage of the full plan costs, or "working rates."

Bi-weekly Co-share Rates

For unions that ratified new CBAs and non-union classified and unclassified (effective January 1, 2025)

For RIBCO (Correctional Officers; Nurses; Civilians) and Non-Classified Union and Non-Union Education

* Salary ranges do not include overtime or other non-salary wages.

** If your scheduled work hours are fewer than the full hours specified for your position, you will be classified as a part-time employee. Your co-share amount is determined according to the full-time annual salary for your job specification, not your part-time wages actually earned.

For unions that ratified new CBAs and non-union classified and unclassified (effective January 1, 2025)

For RIBCO (Correctional Officers; Nurses; Civilians) and Non-Classified Union and Non-Union Education

* Salary ranges do not include overtime or other non-salary wages.

** If your scheduled work hours are fewer than the full hours specified for your position, you will be classified as a part-time employee. Your co-share amount is determined according to the full-time annual salary for your job specification, not your part-time wages actually earned.

* Salary ranges do not include overtime or other non-salary wages.

Historical Rates

Co-Share Rates

- For 26 pay-period classified and unclassified union and non-union employees

- For 20 pay-period classified and unclassified union and non-union employees

- For RITA and State Police Command Staff

Working Rates (full plan costs)

Co-Share Rates

- For 26 pay-period classified and unclassified union and non-union employees

- For 20 pay-period classified and unclassified union and non-union employees

- For RITA and State Police Command Staff

Working Rates (full plan costs)

Co-Share Rates

- For 26 pay-period classified and unclassified union and non-union employees

- For 20 pay-period classified and unclassified union and non-union employees

- For RITA and State Police Command Staff

Working Rates (full plan costs)

In-Network Claims

To view your in-network claims history, please log in to your account at vsp.com.

Out-of-Network Claims

You have two options for submitting an out-of-network claim:

- Complete the VSP Out-of-Network Reimbursement Form and submit to VSP with a copy of your itemized receipt as instructed on the form, or

- Log into your account at vsp.com, complete the online claim form and upload a copy of your itemized receipt.

- VSP does not issue ID cards, but you may print one out after registering/logging into your account on www.vsp.com. Your ID number is your Social Security Number. At your appointment, tell your doctor that you are a member of VSP in order for him/her to verify your VSP eligibility.

Please contact VSP to find a participating doctor or if you have other questions regarding your vision coverage:

- Visit www.vsp.com

- Call 1-800-877-7195